Solar panels (or solar photovoltaics) are finally ready for the advent of the "Golden Age," although many people don't seem to realize it. This will not happen overnight, nor will it be a "great leap forward" development. It will gradually proceed. Here are two basic reasons: 1) In view of the sharp decline in panel prices, solar panels can compete with other forms of power generation in more regions. 2) China is actively expanding the domestic solar market. We find that the concept of grid parity (ie, the cost of solar power generation falls to the cost of traditional power generation) is not without problems. However, the sharp drop in panel prices has led to solar power generation in some regions (these regions have two characteristics, namely high electricity bills and sufficient sunlight) that can already compete with the grid. The territory of these regions will continue to expand, which means that solar power generation in these regions will not be supported by subsidies. China is expanding its domestic solar market and plans to install 21 GW of PV by 2015, a five-fold increase from its original target. According to the GTM Research report: In 2012, solar panel shipments are expected to reach 59GW, but only 30GW of capacity is sold worldwide. As the price of the panel continues to fall, about 21 GW of capacity will be withdrawn from the market in 2015. Please note that the last sentence of the GTM Research report is the same as China's 2015 capacity target data. There should be 42GW "swinging" in the balance between supply and demand, which means that fewer competitors in the market are sharing loot.

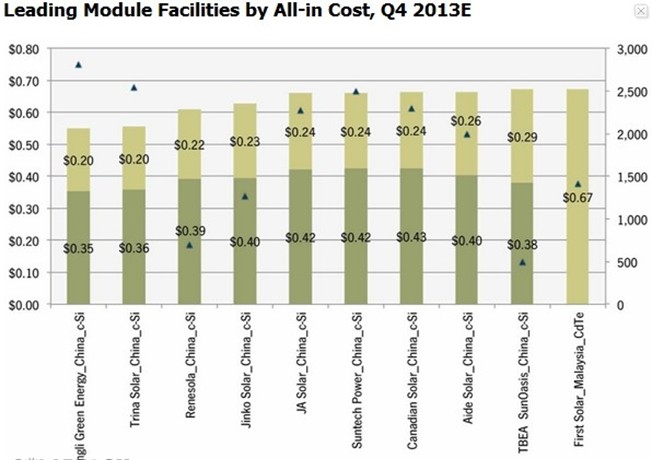

GTM Research predicts that the difficult situation in the photovoltaic industry (currently, almost every manufacturer is in a loss) will last for three years until 2015, until the excess capacity disappears. In fact, we have seen solar companies faltering or delaying the production of new capacity like General Electric. At present, the difficult situation of the photovoltaic industry is caused by overcapacity. Overcapacity has led to a sharp drop in prices (upgrades of more than 50% last year), which has caused many companies to close factories or file for bankruptcy. However, this process will take time. China's huge expansion plan is expected to surpass Germany to become the world's largest solar market, and will further promote the balance between supply and demand. It is predicted that in 2012, the price of photovoltaic polysilicon will drop by 48%, and the price of silicon wafer will fall by 56%. At present, polysilicon is also overcapacity, reducing the total price of solar panel manufacturers (excluding film companies such as FirstSolar). Industry Winners Although the entire industry is not in a good position, the balance sheets of most PV companies are not strong, but not every solar panel manufacturer is going bankrupt. As many companies fail and more companies stop expanding their plans, industry winners benefit from the continued growth of the Chinese PV market and the weaknesses of their weak peers. So, what is the strongest winner? There are two basic conditions: 1) Cost per watt 2) Strength of the balance sheet A company, if it can combine the low cost per watt with the strength of the balance sheet, it is not only possible at present The industry survives in the cold winter, and it is expected to flourish. According to NPDsolarbuzz research, top PV companies are expected to make a profit in 2013. So how do you identify top manufacturers? The standards are not complicated. 2013 Q4 component cost forecast From the above figure, we can see that China's PV companies Yingli Green Energy and Trina Solar are the most efficient, they are the lowest cost solar manufacturers; Yuhui Sunshine, Jinko Energy, Jingao Solar, Suntech Power, Artes, AideSolar, TBEASunOasis and FirstSolar are close behind. Although this is only the forecast for the Q4 cost in 2013, it can be seen that the former “cost giant†FirstSolar will fall out of the top ten. It uses different technologies than other companies in the table. Cadmium-Tellurium (CdTe) batteries are less efficient. Let's take a look at other PV companies. Yingli is expected to become the lowest cost manufacturer by the end of 2013: 1) Q4 in 2011, cash is $669.2 million 2) Debt $2.3 billion 3) Analysts forecast a loss of $0.96 per share this year and a loss of $0.28 per share next year 4) Last year In view of capital expenditures of $769 million, cash flow was negative, totaling $266 million. Trina Solar: 1) Cash $632.5 million 2) Debt $1.14 billion 3) Analysts forecast a loss of $1.05 per share this year and a profit of $0.15 per share next year. 4) Last year, cash flow was positive. However, given the net borrowing of $442 million, the cash flow was only $64 million. From the above short survey, we can see that for the two top solar panel manufacturers (both of which adopt an integrated business model, and part of their cost advantage should come from this), Trina Solar The balance sheet is relatively healthier. Therefore, we can be sure that with the gradual disappearance of overcapacity and the continued expansion of China's PV market, Trina Solar is expected to become one of the photovoltaic companies that will survive this difficult environment and thrive in the next few years.

2013 Q4 component cost forecast From the above figure, we can see that China's PV companies Yingli Green Energy and Trina Solar are the most efficient, they are the lowest cost solar manufacturers; Yuhui Sunshine, Jinko Energy, Jingao Solar, Suntech Power, Artes, AideSolar, TBEASunOasis and FirstSolar are close behind. Although this is only the forecast for the Q4 cost in 2013, it can be seen that the former “cost giant†FirstSolar will fall out of the top ten. It uses different technologies than other companies in the table. Cadmium-Tellurium (CdTe) batteries are less efficient. Let's take a look at other PV companies. Yingli is expected to become the lowest cost manufacturer by the end of 2013: 1) Q4 in 2011, cash is $669.2 million 2) Debt $2.3 billion 3) Analysts forecast a loss of $0.96 per share this year and a loss of $0.28 per share next year 4) Last year In view of capital expenditures of $769 million, cash flow was negative, totaling $266 million. Trina Solar: 1) Cash $632.5 million 2) Debt $1.14 billion 3) Analysts forecast a loss of $1.05 per share this year and a profit of $0.15 per share next year. 4) Last year, cash flow was positive. However, given the net borrowing of $442 million, the cash flow was only $64 million. From the above short survey, we can see that for the two top solar panel manufacturers (both of which adopt an integrated business model, and part of their cost advantage should come from this), Trina Solar The balance sheet is relatively healthier. Therefore, we can be sure that with the gradual disappearance of overcapacity and the continued expansion of China's PV market, Trina Solar is expected to become one of the photovoltaic companies that will survive this difficult environment and thrive in the next few years.  Current ratio and debt-to-cash ratio Analyst Robert Dydo said that Suntech Power and Hanwha New Energy performed best when they combined debt reduction efforts with cash increases. Followed by SolarWorld and Sunpower. Dydo believes that in Q4 2011, the vast majority of solar companies' inventory reductions were 25%. Although Q1 shipments were lower than the expected value of 10% and revenues fell by 20%, we are still optimistic about Trina Solar. Their business in China continues to expand, and two new sales offices have been set up there, and Trina Solar has unveiled its world-recorded HoneyUltra new technology and Trinasmart smart components at this year's Intersolar show in Europe. It is a component-integrated solution that optimizes the power output of a photovoltaic system. In addition, in terms of management, Trina Solar also has an advantage. The following is the opinion of Mike Grunow, Marketing Director of TRW USA: Indeed, Trina Solar is very conservative and economical. During that period, we significantly reduced our debt and built a strong balance sheet to support our products compared to some of our competitors. It is hard not to agree with this point of view. When the situation improves (this will be a gradual process), the company is likely to become the winner in the industry.

Current ratio and debt-to-cash ratio Analyst Robert Dydo said that Suntech Power and Hanwha New Energy performed best when they combined debt reduction efforts with cash increases. Followed by SolarWorld and Sunpower. Dydo believes that in Q4 2011, the vast majority of solar companies' inventory reductions were 25%. Although Q1 shipments were lower than the expected value of 10% and revenues fell by 20%, we are still optimistic about Trina Solar. Their business in China continues to expand, and two new sales offices have been set up there, and Trina Solar has unveiled its world-recorded HoneyUltra new technology and Trinasmart smart components at this year's Intersolar show in Europe. It is a component-integrated solution that optimizes the power output of a photovoltaic system. In addition, in terms of management, Trina Solar also has an advantage. The following is the opinion of Mike Grunow, Marketing Director of TRW USA: Indeed, Trina Solar is very conservative and economical. During that period, we significantly reduced our debt and built a strong balance sheet to support our products compared to some of our competitors. It is hard not to agree with this point of view. When the situation improves (this will be a gradual process), the company is likely to become the winner in the industry.

GTM Research predicts that the difficult situation in the photovoltaic industry (currently, almost every manufacturer is in a loss) will last for three years until 2015, until the excess capacity disappears. In fact, we have seen solar companies faltering or delaying the production of new capacity like General Electric. At present, the difficult situation of the photovoltaic industry is caused by overcapacity. Overcapacity has led to a sharp drop in prices (upgrades of more than 50% last year), which has caused many companies to close factories or file for bankruptcy. However, this process will take time. China's huge expansion plan is expected to surpass Germany to become the world's largest solar market, and will further promote the balance between supply and demand. It is predicted that in 2012, the price of photovoltaic polysilicon will drop by 48%, and the price of silicon wafer will fall by 56%. At present, polysilicon is also overcapacity, reducing the total price of solar panel manufacturers (excluding film companies such as FirstSolar). Industry Winners Although the entire industry is not in a good position, the balance sheets of most PV companies are not strong, but not every solar panel manufacturer is going bankrupt. As many companies fail and more companies stop expanding their plans, industry winners benefit from the continued growth of the Chinese PV market and the weaknesses of their weak peers. So, what is the strongest winner? There are two basic conditions: 1) Cost per watt 2) Strength of the balance sheet A company, if it can combine the low cost per watt with the strength of the balance sheet, it is not only possible at present The industry survives in the cold winter, and it is expected to flourish. According to NPDsolarbuzz research, top PV companies are expected to make a profit in 2013. So how do you identify top manufacturers? The standards are not complicated.

2013 Q4 component cost forecast From the above figure, we can see that China's PV companies Yingli Green Energy and Trina Solar are the most efficient, they are the lowest cost solar manufacturers; Yuhui Sunshine, Jinko Energy, Jingao Solar, Suntech Power, Artes, AideSolar, TBEASunOasis and FirstSolar are close behind. Although this is only the forecast for the Q4 cost in 2013, it can be seen that the former “cost giant†FirstSolar will fall out of the top ten. It uses different technologies than other companies in the table. Cadmium-Tellurium (CdTe) batteries are less efficient. Let's take a look at other PV companies. Yingli is expected to become the lowest cost manufacturer by the end of 2013: 1) Q4 in 2011, cash is $669.2 million 2) Debt $2.3 billion 3) Analysts forecast a loss of $0.96 per share this year and a loss of $0.28 per share next year 4) Last year In view of capital expenditures of $769 million, cash flow was negative, totaling $266 million. Trina Solar: 1) Cash $632.5 million 2) Debt $1.14 billion 3) Analysts forecast a loss of $1.05 per share this year and a profit of $0.15 per share next year. 4) Last year, cash flow was positive. However, given the net borrowing of $442 million, the cash flow was only $64 million. From the above short survey, we can see that for the two top solar panel manufacturers (both of which adopt an integrated business model, and part of their cost advantage should come from this), Trina Solar The balance sheet is relatively healthier. Therefore, we can be sure that with the gradual disappearance of overcapacity and the continued expansion of China's PV market, Trina Solar is expected to become one of the photovoltaic companies that will survive this difficult environment and thrive in the next few years. Current ratio and debt-to-cash ratio Analyst Robert Dydo said that Suntech Power and Hanwha New Energy performed best when they combined debt reduction efforts with cash increases. Followed by SolarWorld and Sunpower. Dydo believes that in Q4 2011, the vast majority of solar companies' inventory reductions were 25%. Although Q1 shipments were lower than the expected value of 10% and revenues fell by 20%, we are still optimistic about Trina Solar. Their business in China continues to expand, and two new sales offices have been set up there, and Trina Solar has unveiled its world-recorded HoneyUltra new technology and Trinasmart smart components at this year's Intersolar show in Europe. It is a component-integrated solution that optimizes the power output of a photovoltaic system. In addition, in terms of management, Trina Solar also has an advantage. The following is the opinion of Mike Grunow, Marketing Director of TRW USA: Indeed, Trina Solar is very conservative and economical. During that period, we significantly reduced our debt and built a strong balance sheet to support our products compared to some of our competitors. It is hard not to agree with this point of view. When the situation improves (this will be a gradual process), the company is likely to become the winner in the industry.Steel Fabrication,Cnc Milling Service,Cnc Fabrication

Machining Parts,Plastic Injection Mould Co., Ltd. , http://www.chmachiningparts.com